Managing the growing problem of underinsurance

Increases in the cost of living and doing business have been rising, and at a faster rate than in many decades.

This is largely driven by supply chain issues and labour shortages during the pandemic, the energy crisis, increases in catastrophe events and inflation.

Each of these events puts a strain on the insurance markets and is reflected in prices, with an increasing risk of underinsurance caused by insured values which are too low.

What does it mean to be underinsured?

Underinsurance in strata occurs when the sum insured on an insurance policy is insufficient to cover the full cost of rebuilding, repairing or replacing the building.

Market value vs replacement value

The market value of a property has no bearing on the price to rebuild it.

The replacement value includes the construction cost, as well as other costs associated with the removal of debris, labour and materials, compliance with current building codes and local council planning provisions, professional fees, taxes and more.

In the current environment of increasing natural disasters, rising labour and building material costs, having adequate insurance in place is more important than ever.

Underinsurance can occur for several reasons.

1. Owners may have carried out renovations and haven’t updated their buildings or contents insurance policy to take account of the additional value.

2. The policy sum insured may not have been reviewed or valued recently so it may not factor in the rising cost of materials if you need to rebuild your property.

3. Owners may not have taken up the suggested increase in building sum insured many insurers propose with the policy renewal called “indexation” to help keep up with the rapid pace of escalating building costs and claims inflation. CHU have seen this in the recent 12 months with 42% of customers maintaining their current sum insured and only approximately 1/3 adopting the suggested indexation on their sum insured. This is largely unchanged from the previous 12-month period despite some significant inflationary pressures over recent times.

4. Some additional costs like debris removal and architects or legal fees may not have been factored into the total cost to rebuild or repair the building.

Unfortunately, many owners corporations* may be unaware of the issue of underinsurance until it’s too late and they’ve suffered a loss.

Why has the problem of underinsurance increased?

Over the last few years, the problem of underinsurance has worsened. This is not entirely the fault of owners corporations. Rather, a set of circumstances that have combined to exacerbate the issue.

• Inflation growth. Central Banks are raising interest rates to try and slow the pace, but the impact on prices is being felt across all sectors of the economy. It’s resulted in replacement costs often being higher than expected.

• Supply chain bottlenecks. The COVID-19 pandemic saw many countries instigate factory closures and port restrictions, which led to shipping congestion and container shortages. This was further hampered by extended worker absences due to isolation rules. The result is an international shortage of materials like timber, steel, cement, metals and plastics, as well as extended delivery timescales.

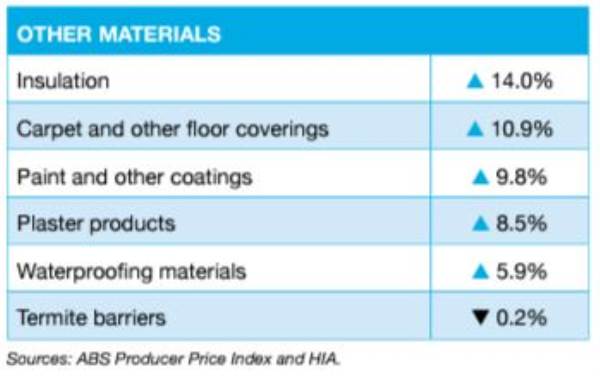

• Rising cost of materials. Shortages and increased demand have combined to increase the cost of most materials. Steel has been the hardest hit, with prices increasing by 42.1% over the 12 months to March 2022 and timber increasing by 20.6%, according to the Australian Bureau of Statistics.

The importance of strata valuations

It’s a legal obligation for an owners’ corporation* to ensure there’s no shortfall for the rebuilding of their strata property because if there is a shortfall, it’s the responsibility of the owners’ corporation to fund the gap. You can find out more about the rules in your state by contacting Fair Trading (or the equivalent government body).

In most states and territories building valuations for strata properties are required by law, but they also make good sense. Typically, they are carried out every two to three years.

An accurate valuation of assets also helps avoid the risk of underinsurance.

What does an insurance valuation cover?

A detailed valuation will account for more than just the replacement value and should include the following.

• The cost of buildings and common property.

• External features like pavements, fencing and recreation facilities.

• Each lot’s permanent fixtures and structural improvements.

• Inflation and cost escalations for labour and materials.

• Professional fees.

• Demolition and debris removal costs.

How to minimise the risk of underinsurance in a strata complex

• Review the building sum insured amount annually (even if you don’t get a new valuation), or consider taking up the insurers suggested indexation because events and factors like material costs could impact your building and repair costs.

• Obtain a new valuation every 2-3 years to assess and value your building’s full replacement and reinstatement cost.

• Factor in all necessary legislative requirements, including the removal of debris, professional fees and taxes, and the escalation of costs during the rebuild.

• Be aware of any undisclosed renovations and improvements by owners. Ensure owners are aware that the owners’ corporation must know about any works within their unit to ensure this forms part of the overall building sum insured.

Article supplied by CHU Underwriting Agencies

Important note

CHU Underwriting Agencies Pty Ltd (ABN 18 001 580 070, AFS Licence No: 243261) acts under a binding authority as agent of the insurer QBE Insurance (Australia) Limited (ABN 78 003 191 035, AFS Licence No: 239545). Any advice in this article is general in nature and does not take account of your personal objectives, financial situation and needs. Please read the relevant Product Disclosure Statement (‘PDS’), Financial Services Guide (‘FSG’), and the Target Market Determination (‘TMD’) which can be viewed at chu.com.au or obtained by contacting CHU directly. * The Owners’ Corporation also known as: Body Corporate, Strata Company or Strata Corporation.

View Comments

(0)